International Taxes for US Citizens

Residency vs. tax residency for U.S. retirees abroad, in plain English: golden visas, the 90-day bounce, Mexico's unique edge, and how the ads mislead you.

Below the text conversation is a type of calculator to assess taxes, Cost of living, Quality of life, Healthcare and Visas for various countries.

Intl.Residency vs. Taxes: The issues the Expat Advertisments Don't Want You to See

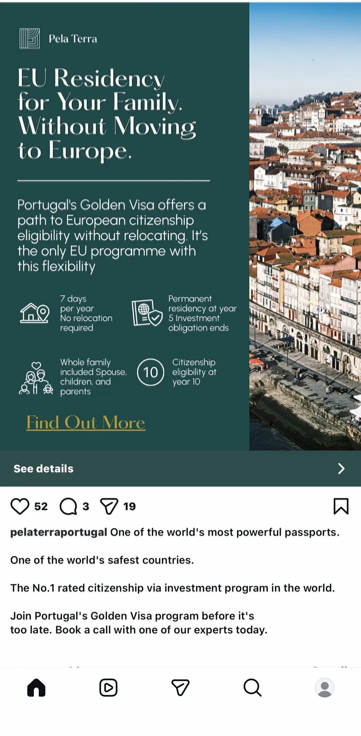

If you spend any time researching life abroad, your feed fills up with the same glossy pitch. A recent one I came across is a good specimen: a polished ad from a Portugal Golden Visa promoter, headlined "EU Residency for Your Family. Without Moving to Europe," with tidy icons promising "7 days per year — no relocation required," "permanent residency at year 5," "citizenship eligibility at year 10," and "whole family included." The caption: "One of the world's most powerful passports… join before it's too late."

None of those individual claims is technically false. And that's exactly what makes the genre so effective — and so misleading. These ads work by blurring two things that are completely separate: a residence permit (immigration status) and tax residency (where you actually owe income tax). Once you separate them, the whole tax/residency landscape gets simple - well kind of .hahaha. It never does for a US citizen - so think twice before you want to get your US citizenship or greencard. I have tried to create some clarity around it but it's a maze of rules and stages for every country. The more poor you are the easier, or if you are mega wealthy say over $10M in liquid net worth but between say $250k- and $3M in liquid networth assets and over a certain age like arond 50yo it becomes painful. You are basically tied to the US system and its very difficult to escape without paying much of your hard worked savings away to both countries.

The one rule that unlocks everything: A residence permit lets you legally be in a country. Tax residency — which is what determines whether that country taxes your income — is triggered by actually living there, usually by spending 183+ days a year or making it your real home. They are not the same thing, and one does not automatically create the other. This is not a hard and fast rule for every country, so you need to be very careful depending on how you pursue your international dream.

And one fact that applies to every option below:

As a U.S. citizen, you file and owe U.S. federal tax no matter where you live.

The Foreign Tax Credit rule/law lets foreign tax offset your U.S. bill, but it can't make your total go below your U.S. baseline. So the question is never "how do I pay zero tax" — it's "do I also pay a second country a little bit more to negate the US tax bill, and what do I get for it."

The four (and a half) options

Almost every arrangement people and vendors like above pitch you is a version of one of these. Each is a different trade-off between money, physical presence, and tax. There maybe slight variations but if they seem too good to be true they probably are, so be very cautious.

1. Move there and become a full-time resident

You get an inexpensive, income-based residence visa and actually live in the country.

- What it is: A passive-income or "retirement" visa that asks you to prove steady income, not park a lump sum investment.

- Examples: Portugal D7 (~€920/month of passive income), Spain Non-Lucrative Visa (~€2,400/month plus private health insurance), Greece Financially Independent Person visa (~€3,500/month), Italy Elective Residence visa (~€31,000/year), Mexico Temporary/Permanent Resident (savings or income proof).

- The presence requirement: You're expected to actually live there — Portugal's D7, for instance, requires ~183 days a year and forbids long absences.

- The tax reality: Living there makes you a tax resident, so your worldwide income is taxed locally — in post-NHR Portugal or Spain, that runs up to ~48%. The U.S. Foreign Tax Credit prevents true double taxation, but you pay the higher of the two bills.

- Best for: People who genuinely want to live somewhere for the lifestyle, healthcare, and community — and who accept the tax that comes with it.

2. Hold residency but deliberately stay under the tax line

This is the Golden Visa model — and the one the ads are selling.

- What it is: You make a qualifying investment, receive a residence permit, and stay just long enough to keep it without ever becoming a tax resident.

- Example: Portugal's Golden Visa — now ~€500,000 into a regulated fund (the real-estate route ended in October 2023), requiring only ~7 days per year in the country. Greece is still has a Real Estate option for €250,000 but only in certain areas or renovated buildings. So this is a bit less risky than a pure investment Golden Visa Play as is the case in the Ad above and what is required in Portugal.

- The tax reality: Because you barely set foot there, you never become a tax resident, so the country taxes none of your worldwide income. You remain a U.S. tax resident, taxed by the U.S. as always.

- What you're actually buying: Not a tax break and not a place to live — optionality. The right to move to the EU later, Schengen travel, family inclusion, and a path to a passport. It's a "Plan B" insurance policy for people with capital to spare.

- The catch: ~€500,000 locked in an illiquid fund for 5+ years (real investment risk — these can lose money), plus tens of thousands in fees. And the moment you'd actually move there to enjoy it, you become a tax resident and option #1's tax bill switches on. You can't have "live in Portugal" and "pay no Portuguese tax" at the same time.

3. Don't get a visa at all — bounce on tourist allowances

The maximum-flexibility, zero-cost path.

- What it is: Live on the visa-free tourist windows and rotate between countries so you never become a resident anywhere.

- How the limits work: The Schengen zone gives Americans 90 days in any 180-day period across the whole bloc (not per country). You stack that with non-Schengen places that allow longer stays.

- Examples of longer visa-free stays for U.S. passports: Georgia (up to a year), Albania (a year), the U.K. (six months), Ireland (90 days, and outside Schengen so it doesn't burn your Schengen clock), Mexico (up to 180 days), plus the Balkans and others at ~90 days each.

- The tax reality: You're a tax resident nowhere abroad, so you owe only your U.S. baseline. No foreign income tax, no lock-up, no paperwork.

- The catch: Logistics. You're tracking day-counts, packing and moving, and renting short-term. (Note: Romania, Bulgaria, and Croatia are now in Schengen, so they count against your 90/180.)

- Best for: People who value freedom and dislike commitment — this is the "perpetual traveler" approach, and it's the one our interactive tool's Perpetual Traveler tab is built to plan.

4. The investment / "citizenship by investment" play

A close cousin of #2, but worth calling out separately because it's an asset purchase, not a relocation.

- Golden/residency-by-investment visas (Portugal, Greece, etc.) buy you a residence permit and a slow path toward citizenship.

- Citizenship-by-investment programs (Malta, several Caribbean nations) sell you a passport more directly, for a larger sum.

- Reality check: You're buying a document — mobility and a backup nationality — not a tax outcome or a home. Evaluate it like any illiquid, long-horizon investment, not like a vacation.

…and a half: a few routes the ads skip

- Territorial-tax countries. Some places tax only locally-sourced income, so you can become a full resident and still owe no local tax on your U.S. pension, dividends, or gains. Examples: Panama, Paraguay, Costa Rica, Georgia, the UAE, Thailand's LTR visa. This is the genuine "live there and low tax" sweet spot — and notably, no EU country offers it, because EU members tax worldwide income.

- Citizenship by descent (ancestry). If you have a qualifying Italian, Irish, Polish, or other ancestor, you may be able to claim an EU passport with no investment and no residence requirement at all — the cheapest, most flexible route of all, if you're eligible.

- Digital nomad visas (e.g., Portugal's D8). Cheaper than a Golden Visa, but built for remote workers with an income threshold, and they generally require residence — which means tax residency. Not a retiree tool.

Mexico: the one that's genuinely unique — and only for retirees

Mexico deserves its own box, because it pulls off something no other popular destination does. But it only works if your income looks like a retiree's, so read the whole thing before you bank on it.

Start with what Mexico is not: it is not a territorial-tax country. A Mexican tax resident is taxed on worldwide income, progressively up to 35% — foreign income included. On paper, that looks like Option 1 above.

The twist is how Mexico decides who counts as a tax resident. It doesn't use a day-count for individuals the way most countries do. You're a tax resident if your home is in Mexico — but if you also keep a home in another country, the tiebreaker is your "center of vital interests," which lands in Mexico only if more than half your income is Mexican-source or your main profession is in Mexico.

For a retiree, neither is ever true:

- Your income — pensions, Social Security, IRA and brokerage withdrawals — is 100% U.S.-source.

- You have no profession in Mexico.

So even living in Mexico full-time on a Temporary or Permanent Resident visa, your center of vital interests points away from Mexico, you are not a Mexican tax resident, and Mexico taxes none of your foreign income. A U.S.–Mexico tax treaty (1994) reinforces the tiebreaker, and enforcement against foreign retirees' foreign income has historically been light.

The result is a pairing almost nowhere else offers:

- You actually live there — cheap, easy residency; unbeatable proximity to the U.S.; low cost of living; strong, affordable healthcare.

- And your foreign income goes untaxed locally — the outcome you'd otherwise only get in a territorial country like Panama.

Everywhere else forces a choice between those two: live there or avoid the local tax. Mexico, for a retiree, gives you both. That's a big part of why it consistently tops the list of U.S. retirement destinations, and why it belongs in a category of its own.

Why "only for retirees." This works precisely because your income is foreign passive income. A remote worker, a consultant with active clients, or anyone earning Mexican-source income would trip the trigger and become taxable on worldwide income. The advantage is a quirk of the residency rules meeting a retiree's all-foreign income profile — change the income profile and it evaporates.

The caveat — don't skip this. This is not a codified exemption like Panama's territorial system. It rests on the center-of-vital-interests test, the treaty, and light enforcement — not a law that says "retirees don't pay." It's strongest when you keep ties or a home elsewhere, so the two-homes tiebreaker keeps working in your favor. If you give up your U.S. base entirely and make Mexico your only home, the "home in Mexico" prong can make you a tax resident on its own, and the protection weakens. It is a favorable gray zone, not a guarantee — confirm your exact circumstances with a cross-border tax advisor before you rely on it.

Where it sits on the map: Mexico is a hybrid of Option 1 (live there full-time on a cheap visa) and the territorial sweet spot (foreign income untaxed) — achieved through a forgiving residency rule rather than a written exemption. Unique among the popular destinations, and specific to a retiree's foreign-income profile.

How the ads mislead you — line by line

Using that Portugal Golden Visa ad as the example, here's the sleight of hand:

- "EU residency without moving." True, but it's selling you a permit you barely use, while the phrasing implies you get the benefits of living in Europe — the healthcare, the lifestyle, the cost of living — without moving. You don't. You get a card in a drawer and Schengen travel.

- They never mention tax — on purpose. The unspoken catch is that the "no tax" only holds because you don't live there. Actually move in to enjoy the place, and you become a tax resident facing rates up to ~48%. The ad sells the residency and stays silent on the trap on the other side of it.

- "Citizenship eligibility at year 10." It dangles the passport while burying the conditions: you must maintain the investment the whole time, pass a language test, and clear long bureaucratic backlogs — and Portugal has proposed legislation to extend the naturalization timeline from five years toward ten. The clock they're showing may be getting longer, not shorter.

- The capital lock-up and risk vanish. "Invest €500,000" sounds like buying an asset. It's locking half a million euros in an illiquid private-equity or venture fund for 5+ years that can lose money. That risk never appears in the icon list.

- Manufactured urgency. "Join before it's too late" is a sales trigger, not a deadline. The program has survived years of "it's ending!" headlines.

- The conflict of interest. The firms running these ads typically earn fees placing your money into the very funds they recommend. They are salespeople, not neutral advisors.

- True-but-irrelevant flexing. "One of the world's most powerful passports / safest countries" is accurate and completely beside the point of whether this product fits your life.

None of this means the Golden Visa is a scam — for the right person (someone wealthy who wants an EU Plan B without moving), it's a legitimate, well-defined product. The dishonesty is in the framing: pricing optionality as if it were lifestyle, and selling residency while hiding the tax it implies.

A simple way to decide

Match the tool to what you actually want:

- You want to live somewhere for the life it offers → a cheap income-based residence visa (option 1). Accept the local tax — or choose a territorial-tax country so there isn't any.

- You want an EU passport or a Plan B without moving → a Golden Visa (option 2/4). Expensive, no tax, no lifestyle. Treat it as an investment.

- You want freedom and hate commitment → don't get a visa; bounce (option 3). Only your U.S. tax follows you.

- And remember the floor: because the U.S. taxes you wherever you go, a "low-tax" foreign country rarely saves a U.S. citizen money on tax — the real lever is cost of living, not the headline rate. (That's exactly what the spending-power model on this page is built to show, including the difference between a full-resident scenario and a sub-183-day "snowbird" one.)

This is general information, not tax, legal, or immigration advice. Visa rules, income thresholds, day-counts, and tax treaties change frequently and vary by your exact situation. Confirm anything you'd act on with a qualified cross-border tax advisor and immigration lawyer before committing money or signing anything.

International Living — Tax & Spending Power Model

Enter a portfolio, profile and budget once. The model computes the U.S. baseline federal tax you can't escape as a citizen, then ranks 34 residency options by what actually moves the needle — local spending power after the Foreign Tax Credit, not the headline tax rate. A second tab plans a no-commitment perpetual-traveler rotation.

⚠ Directional planning tool — not tax advice. Confirm any move with a cross-border specialist.The Foreign Tax Credit sets a floor.

▸ Tap any country to expand the plain-English breakdown. The slider above re-weights the Composite score between money and lifestyle.

| # | Country | Net tax | After-tax $ | COL (US=100) | Local spending power (US=100) | QoL | Composite |

|---|

Instead of committing to one country, rotate through several — staying under 183 days in each so no country can claim you as a tax resident. You owe only the U.S. baseline (~no foreign income tax), and you steer your budget toward low-cost regions. The trade-off is logistics and tracking your days, especially Europe's 90-in-180 Schengen window.

How the numbers work & what the model simplifies

Net tax = foreign tax on active-band income plus residual U.S. tax after the Foreign Tax Credit: foreign + max(0, US baseline − foreign). The FTC offsets U.S. tax dollar-for-dollar, so your total never falls below the U.S. baseline — any country taxing below that rate saves nothing on tax.

Snowbird mode assumes you stay under ~183 days everywhere and never become a foreign tax resident, so foreign tax is $0 and every country's net tax equals the U.S. baseline. The ranking then turns purely on cost of living.

Local spending power = after-tax dollars × 100 ÷ cost-of-living index, re-indexed so U.S. after-tax power = 100. Composite = spending power × (QoL ÷ 10). QoL scores are subjective first-pass estimates — re-weight to your own priorities.

U.S. tax uses 2025 single-filer brackets; LTCG uses the 0% bracket up to ~$48,350 of stacked ordinary income. Roth withdrawals are excluded from taxable income. State tax is not included (FL/TX/NV/WA = $0). Wealth/estate taxes are flagged per country, not added to the headline number. COL indexes are approximate Numbeo-2026 national averages calibrated to US=100 — real expat costs in capitals run 20–50% higher. Tax brackets reflect 2024–25 rates; re-verify for your move year.